Published on April 30, 2018

Yuri Ivanov

Last year I have published an article about Russian market of amino-acids and about Russian market of L-Lysine in particular.

It was noted that Russia was rapidly increasing the importation of Lysine in the last years. Also the plans of local companies to start their own production of Lysine were indicated.

Though only few months have passed after this article publication the significant changes took place at Russian Lysine market which will be shown below.

1. General Information

L-lysine is 2,6-di amino hexane acid with the chemical formula NH2(CH2)4CH(NH2)COOH. It is one of the major amino acids for animal feed.

Lysine is mainly consumed by pig-breeding farms (55% of the total consumption) though it is also used for feeding the chicken, ducks and turkey.

The world consumption of Lysine is estimated as 2.4 mMT (2017)

The largest world Lysine manufacturer and exporter is China: Chinese Lysine production capacity exceeds 1.8 mMT/ann, while the local consumption is approximately 700 kMT/ann (2015).

The raw material for Lysine is corn. One tone of corn gives 250 kg of Lysine.

Amino acids are the key feed components and thus the world demand of Lysine grows as the demand of Amino Acids grows in general. According to estimations the world population will grow to 9 Billion by 2050 which results in growing demand of food and consequently in growing demand of animal feed.

2. Local Demand In Russia

In 1990s and early 2000s most of meat was imported to Russia from abroad and thus there were no demand of Amino Acids. Later on the demand of Amino Acids started growing and it grew nearly from zero in early 2000s to 200 kMT/ann in 2016 of which 140-150 kMT was the demand of Lysine.

The exact importation figures are not available since part of Amino Acids is imported to Russia in the form of premixes which have a different HS code in importation statistics.

Russian customers consume different forms of lysine: in addition to Monohydrochloride form with the L-lysin content of 78-79% there are such forms as Lysine Sulphate 65% (< 51% of L-Lysine) and Lysine Sulphate 70% with not less than 55% of pure L-Lysine.

The differences in pure lysine content in the different forms could be the reason of additional deviations in the estimated consumption and importation figures.

The biggest consumers of Lysine are the agriholdings like Koudice MKorma (the JV of Russian MKorma and Dutch De Heus), Megamix, Provimi (the brand of Cargill), Miratorg, Agrobalt Trade, Aleiskzernoprodukt, Reifeissen Agro, DSM Nutrition and others.

3. Local Production Of L-Lysine in Russia

Premix Plant №1

Premix Plant №1 was the first local producer of Lysine in Russia. It started in September 2015 in Belgorod Area. Now it produces 57 th MT/ann of lysine sulfate (equivalent to 35 th MT of lysine chloride in crystal form). Byproducts are starch (23 th MT), bran (39,6 th MT) and gluten (20,8 th MT). The owner is Prioskolyie Group of companies and 40% of Lysine goes to own Group needs while 60% is sold to the market.

AminoSib

The second Russian Lysine production is AminoSib which started in December 2017 in Ishim of Tumen Area. AminoSib belongs to Jubileyny agriholding and targets to produce 30 kMT/ann of Lysine sulfate.

Jubileyny owns 50 thousand heсtarеs of land where it produces 100 kMT/ann of corn half of which is used for the feed directly and another half is consumed as a raw material for Lysine production.

50% of Lysine production will be used for own need of Jubileyny (it owns swine number of 100 thousand) and 50% will go for export.

Besides own raw material base Jubileyny's competitive advantage is electricity which is half cheaper than in other regions.

Before starting own Lysine production Jubileyny was distributing Chinese Lysine and thus collected a vast market experience and created the distribution channels.

DonBioTech-Evonik

The joint plans of Evonik Industries and DonBioTech for building up a Lysine plant in Donen Rostov area were announced yet in 2012.

According to the plans a new plant was scheduled to go on stream in 2014 with a capacity of around 100,000 metric tons of Biolys® , own Evonik brand of granulated Lysine sulfate. It was also planned that the plant will produce 25 kMT/ann of Gluten and 100 kMT/ann of the feedstuff.

The start of a new plant was postponed many times. The target capacity of the new plant was also corrected from 100kMT/ann to 85 kMT/ann.

Among the reasons for delay there were mentioned difficulties in financing caused by Ruble devaluation in 2014 and technological restrictions caused by anti-Russian sanctions. Some reviewers do not exclude the effect of certain specific non-market circumstances which foreign investors often face when doing business in Russia.

The latest dates of the plant start were announced as August 2017, then again it was postponed till February 2018 but still it is told that the plant is ready only 70%. In addition the construction of the road from DonBioTekh to Rostov highway is frozen.

The project remains nevertheless to be very promising for implementation first of all due to availability of corn which is the raw material for Lysine manufacturing. For realization of its production plans Biotekh would need 250 kMT of corn annually.

The total corn harvest in Donen Rostov Area was 12 mMT in 2017. More than enough.

4. Importation Of L-lysine To Russia

Since recently here were no own production of Lysine in Russia and the importation of Lysine grew as grew the production of meat.

The biggest supplier country was China:

The major importer companies were: De Heus, Megamiks, VlasAgro, Provimi and Tcherkizovo.

The situation changed when Premix Plant No 1 have launched the production in the end of 2016. In the second half of 2017 Russian Federal Service On Veterinary and Phitosanitary Control (Rosselkhoznadzor) has banned the importation from 6 Chinese plants who were the biggest importers of Lysine to Russia.

In number of banned were Eppen Group, Meihua Group and Golden Corn .

The officially announced reason was the refusal of Chinese plants to allow the inspection at their own production by Russian authorities. But one could guess this decision was made to support the local producers.

The stop of Chinese importation have caused the drop of Lysine importation in the 4th Q 2017:

The importation in the 1st Q 2018 was also much lower compared to 1st Q 2017:

As a consequence the importation geography changed and Indonesia became the leading importer of Lysine to Russia:

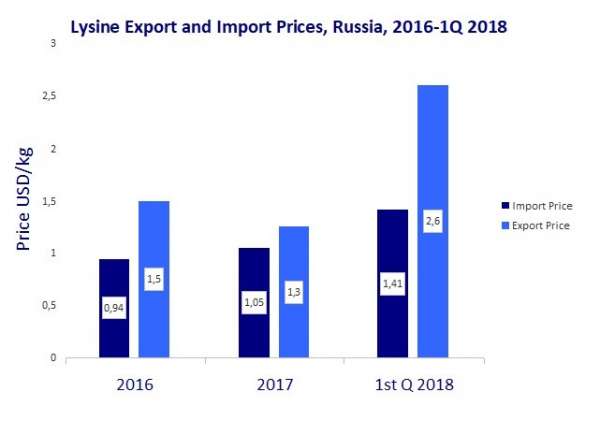

5. Importation Prices

The start of own Russian local Lysine producers has effected the importation Lysine prices:

6. Chinese Producers Do Not Give Up

But Chinese Lysine producers did not give up after their exportation to Russia was banned. To compensate the losses the Chinese producers are studying the possibility to open the local manufacturing of L-Lysine in Russia.

Besides the compensation of importation losses another reason of localization plans is the price of corn which is much cheaper in Russia compared to China.

The corn production in Russia is growing: the 2017 harvest is estimated as 135 mMT. So there will be no problems with the cheap raw materials.

Chinese investors consider Siberia and Altay regions as the possible Areas for the new plants since these regions are located close to corn production.

7. Now What?

Corn Derivative Instead Of Corn

Agriculture is a growing industry in Russia. The corn harvest in 2017 reached 135 mMT. The growth rate in corn production in Russia (13%) exceeds the world growth rate (2%) . The grain stock is also growing while the grain elevator capacities are limited. Corn producing companies are no longer satisfied with just exportation of corn and they are thinking of extracting more profit out of each kg of raw material by implementation the deep corn processing projects.

The total amount of compound animal feedstuf production might be expected to reach 50 mMT/ann in 2021 and some experts think it is a very moderate forecast.

The demand in amino-acids and in l-Lysine in particular will grow in Russia even faster than the growth of animal feed production in general.

Lysine Sulfate Or Lysine Chloride?

The advantage of Lysine Sulfate is the lack of Chlorine and the presence of related substances like organic acids, mineral salts and amino acids.

The same time the advantage of Lysine Chloride is the opportunity to use less product due to higher pure Lysine content and better produceability which makes Lysine Chloride the product preferred by the technologists.

All the 3 mentioned Russian local Lysine producers produce (or will start producing as DonBioTekh) Lysine Sulfate which keeps the door open for the importation of Lysine Chloride.

Thus it is very questionable that the local production of Lysine will totally supersede the importation in the near future. Unless some new market player launches Lysine Chloride production plants.

This new potential investor will gain a huge market advantage because the local corn, working power and electricity are cheap and there is no existing local Lysine Chloride production. But this new potential investor will succeed only in case when he finds out the reliable local partner who could help to clear the local administrative barriers including the specific non-market forces mentioned above.

04.05.2018, 4076 просмотров.