6 October 2016

Russian grain crop exceeds expectations

At the beginning of 2016, new Russian crop prospects looked promising but the reality exceeded expectations. Despite the bumper crop, the country is exporting grain at a slow pace.

Mr Andrey Sizov Jr, SovEcon Managing Director

External Contributor

The 2016 harvesting campaign is almost over in Russia. As of 27 September, farmers harvested 109.8Mt of grain in bunker weight from 41.9Mha, accounting for 89% of the planted area. This includes 74.2Mt of wheat from 26.3Mha (95% of area) and 18.6Mt of barley from 7.9Mha (95%). Maize is the only crop for which forecasts may yet change noticeably, with around 3Mt of maize harvested from 0.6Mha (21%).

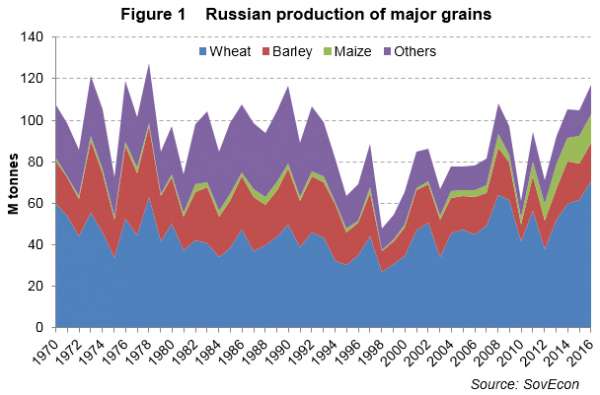

Our latest forecast of total grain and pulses production is 117.2Mt, up 12% year on year (YoY). Within this total, the wheat crop is forecasted at 70.8 Mt (+15% YoY), with barley output at 18.5Mt (+5% YoY) and maize production at 13.8 Mt (+5% YoY). If these forecasts are met, the total grain crop will be the highest since 1978 when the country harvested 127.4Mt of grain and the wheat crop will set a new record (Figure 1). Maize production is also expected to surpass the previous record of 13.2Mt, which was set in 2015.

Figure 1 Russian Production Of Major Grains

Yields are significantly above expectations

Four months ago, we were already projecting a bumper grain crop (read more here) due to good crop conditions. Barley and maize forecasts have remained almost unchanged since that time. However, since May, the wheat crop forecast has been revised up significantly, from 61.1Mt to 70.8Mt.

The total wheat area came in higher than expected at 27.7Mha, compared to the 26.2Mha forecast in May. This is because of higher spring wheat planting (13.7Mha vs 13.0Mha in May) and unexpectedly low winter kill, which resulted in an increase of winter wheat area to 14.0Mha (13.2Mha). For harvest 2016, the winter kill rate is only 3.7%, compared to 12.5% for harvest 2015 and roughly two times lower than the average for the previous 5 years.

In May, we were using wheat yields "close to, or slightly above the average" but warned that these numbers "may still be conservative". Indeed, 2016 wheat yields surpassed all expectations and this became the major driver boosting the current crop size. Enough heat and a lot of rains at close to optimal timing (contrary to France) had a very positive effect on wheat yields. In the majority of regions in the European part of Russia, wheat yields are close to or set new records.

The current Russian average wheat yield is 2.8t/ha (+9% YoY). The increase is noticeable but not that impressive. However, if we look at particular Federal Districts (FD), the difference is much more noticeable. Average yields in the Central FD are 3.8t/ha (+20% YoY) and 2.2t/ha in the Volga FD (+25% YoY). In the South FD, which is the top wheat producing and exporting district, yields are averaging 4.2t/ha (+13% YoY).

Asian regions of Russia, mainly producing spring wheat, show more average results for this crop. Yields in Siberia are 1.6t/ha (+2%), in the Urals are 1.7t/ha (unch).

The higher yields led to a significant increase in wheat production in the European part of Russia (Figure 2). Production in the Asian part, growing mostly less productive spring wheat and for which delivery to export terminals is too expensive, keeps stagnating.

Figure 2 Russian Wheat Production By Federal District

So far exports are slow for the bumper crop...

Despite a bumper crop, grain and wheat exports from the country are proceeding at a relatively slow pace. According to official customs data, exports of major grain crops (wheat, maize and barley) in the first two months of the season (July-August) were 5.4Mt, which is close to the figure of the previous year (-1% YoY). Wheat exports in July and August 2016 totaled 4.6Mt, up 11% or 0.4Mt on July and August 2015. At the same time, total grain output is expected to exceed previous year by 12 Mt and wheat crop by 9 Mt.

However, similar to 2015/16 official exports data on wheat is likely to be misleading. In our article for AHDB in December 2015 (read here) we noted the difference between actual and reported shipments. The major reason was delays in customs reporting due to the wheat export tax. Customs allowed cargo to pass, waited for additional documents from exporter confirming the reported export prices and only afterwards issued permanent customs declaration, which are used as the basis for calculation of export volumes. We spotted the difference looking at data from ports on vessels line up and customs' information.

By the end of 2015/16, customs data had caught up with actual export volumes. This season, with wheat exports increasing rapidly due to the arrival of the new crop, this difference is happening again. SovEcon estimates wheat exports in July-August at 5.5Mt, however, even this revised figure is relatively low for a current record crop. It is slightly below our estimate of exports in July-August 2015 of 5.6 Mt and significantly below July-August 2014 when Russia exported 6.9Mt.

In first 3 months of 2016/17, we expect wheat exports to be around 9Mt (Figure 3) and grain exports around 10.6Mt. Those figures are close to the previous year's pace and well below 2014/15.

Figure 3 Cumulative Wheat Exports From Russia

There are several factors behind the relatively slow start of the export season. Traders were more cautious about selling the new wheat crop during the summer amid rainy weather, fearing potential issues with quality. Another reason is that several large trading houses made huge losses on grain exports at the end of the previous season when the domestic market strengthened unexpectedly for many market players.

Rising domestic milling wheat prices has also been a factor. Farmers have been selling milling wheat unwillingly amid widespread (and somewhat exaggerated, in our view) talks of the low quality of the new crop. This coupled with a relatively strong exchange rate for the ruble decreased the competitiveness of Russian wheat in the export market.

September wheat exports were also negatively affected by Egyptian ergot saga. No shipments were conducted to the largest market for Russian wheat in the first 3 weeks of September, as a requirement of zero ergot, introduced at the end of August, couldn't be met. More recently Egypt has cancelled its zero ergot policy and straight afterwards GASC purchased 240Kt of wheat from Russia.

...but Russia is expected to remain an aggressive seller

Despite the slow start, at SovEcon we still expect Russia to set a new record of wheat and grain exports this season. Total grain and pulses exports are forecast at 40.7Mt, including wheat exports at 30.4Mt.

To meet that target, Russia has to be an aggressive wheat sellerduring the rest of the current season. Contrary to previous years, when the country was selling two-thirds or more of the total export volume during the first half of the season, this season there will be still a lot of wheat to offer in the second half of 2016/17.

Russian wheat is also likely to gain a larger share in some countries or enter new markets. Algeria and Morocco, with forecast combined imports of 13.2Mt this season, mostly buy wheat from France. In the current season, amid the poor French crop, they will have to increase purchases of wheat from other suppliers, including Russia. So far, deliveries to Algeria have been modest, only 22Kt in July-August (customs' data) vs none in previous years. To date, Morocco has already purchased 181Kt from Russia, which is already one and a half times higher than the total for the whole previous season.

Another important destination this season is likely to be South East Asia. Due to the relatively low average quality of the 2016 crop, Russia is expected to export more feed wheat or low quality milling wheat to destinations like Bangladesh, Philippines, Thailand or Indonesia. India, which purchased a small cargo of 3Kt in August, could also be a big importer of Russia wheat after the recent decrease to its import tax.

Concluding comments - Wheat tax lifted but risk of the government limiting exports remains high

On 27 September the wheat export tax, introduced in July 2015, was lifted by Russian authorities. Recently, the tax hasn't had a noticeable effect on exports, as it was only 10 rub ($0.16)/t. If it hadn't been lifted, the tax could potentially have affected exports later in the season if world prices increased and/or the ruble devaluated. Read more on the tax mechanism here.

The tax hasn't been completely removed but set to zero until July 2018, when authorities are expected to review it. However, fortunately for wheat growers around the world, except Russian ones, the decision doesn't guarantee that the government won't attempt to limit exports if there is a view that the export pace is too high. Recent history shows that Russian authorities, encouraged by influential livestock lobby, don't hesitate to intervene in the market.

At least in the medium term, this factor, in addition to weather surprises and low prices, is expected to remain one of the key obstacles in Russia's way to becoming a larger grain grower and exporter.

Key points

Russia is to harvest bumper grain crop and record wheat crop

Start of the export campaign is relatively slow but the country will remain an aggressive seller during the rest of the season

The wheat export tax is set to zero but the risk of government intervention remains high

06.10.2016, 2641 просмотр.